IEA WEO 2022 – Nuclear Generation Could More Than Double By 2050

The International Energy Agency (IEA) released on 27 October the World Energy Outlook 2022.

The report considers the ongoing global energy crisis as a “historic turning point towards a cleaner and more secure energy system”, thanks to the unprecedented response from governments around the world, including the Inflation Reduction Act in the United States, the Fit for 55 package and REPowerEU in the European Union, Japan’s Green Transformation (GX) programme, K-Taxonomy, aiming to increase the share of nuclear and renewables in Korea’s energy mix, and ambitious clean energy targets in China and India.

The report analyses different scenarios:

- Net Zero Emissions by 2050 Scenario (NZE) sets out what needs to be done to move beyond announced pledges towards a trajectory that would reach net-zero emissions globally by 2050.

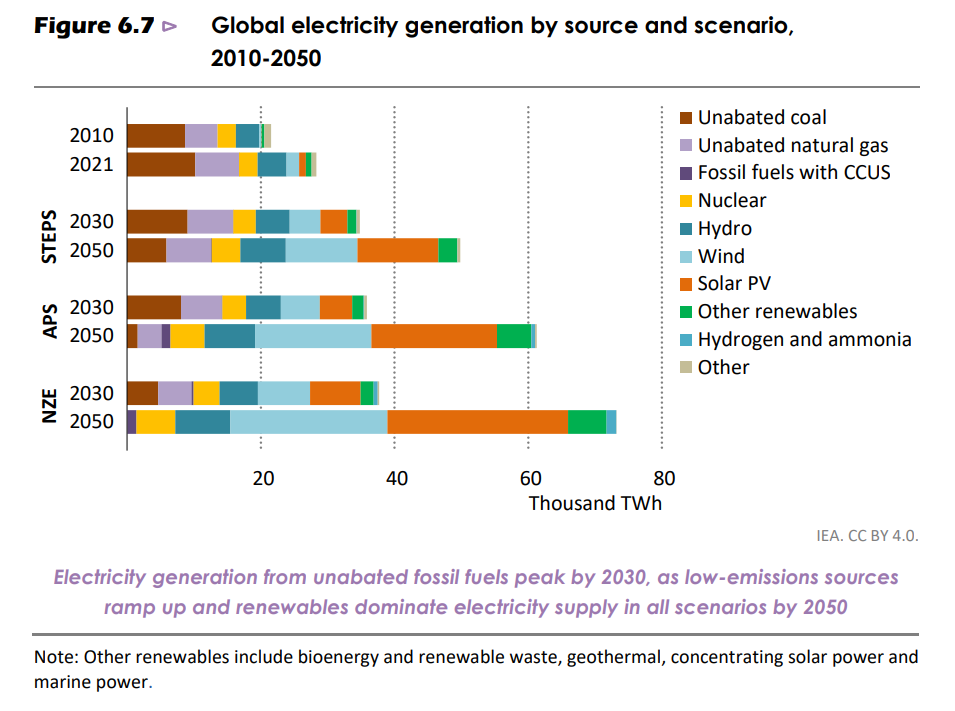

- Stated Policies Scenario (STEPS), representing a path based on the energy and climate measures governments have actually put in place to date, as well as specific policy initiatives that are under development.

- Announced Pledges Scenario (APS), which maps out a path in which the net zero emissions pledges announced by governments so far are implemented in time and in full.

“For the first time ever, a WEO scenario based on today’s prevailing policy settings – in this case, the Stated Policies Scenario – has global demand for every fossil fuel exhibiting a peak or plateau,” the IEA said. In this scenario, there is a reduction in the use of coal within the next few years, natural gas demand reaches a plateau by the end of the decade, and rising sales of electric vehicles mean that oil demand levels off in the mid-2030s before ebbing slightly to mid-century.

The share of fossil fuels in the global energy mix in STEPS falls from around 80% to just above 60% by 2050. The declines are much faster and more pronounced in the WEO’s more climate-focused scenarios.

Nuclear energy continues playing a key role in energy transition, decarbonisation of economies and reduction of CO2 emissions.

New nuclear projects, programmes, and investments, as well as lifetime extensions for operational nuclear power plants in advanced economies, are both crucial in helping limit global emissions.

In the STEPS scenario, global nuclear output increases from 2776 TWh in 2021 to 3351 TWh in 2030 and to 4260 TWh in 2050. However, nuclear maintains its current share of about 10% in total electricity generation. This scenario requires the completion of 120 GW of new nuclear capacity by 2030, as well as the addition of another 300 GW worth of new reactors between 2030 and 2050 in over 30 countries.

In the STEPS scenario, global nuclear output increases from 2776 TWh in 2021 to 3351 TWh in 2030 and to 4260 TWh in 2050. However, nuclear maintains its current share of about 10% in total electricity generation. This scenario requires the completion of 120 GW of new nuclear capacity by 2030, as well as the addition of another 300 GW worth of new reactors between 2030 and 2050 in over 30 countries.- In the APS scenario, around 18 GW of new nuclear capacity is added per year over the outlook period, over a quarter more than in the STEPS, but the higher level of electricity demand in this scenario means that the nuclear share of the electricity supply mix remains about 10%. In APS, nuclear generation increases to 3547 TWh in 2030 and to 5103 TWh in 2050.

- In the NZE scenario, lifetime extensions in the 2020s helps limit global emissions, and an average of 24 GW of capacity added each year between 2022 and 2050 more than doubles nuclear power capacity by 2050. In this scenario, nuclear generation increases to 3896 TWh in 2030 and to 5810 TWh in 2050. However, nuclear’s share of the electricity mix declines to 8% in 2050 due to very strong growth in electricity demand in the NZE scenario.

The WEO 2022 also noted that investment in nuclear power is “coming back into favour” in some countries.

There have been announcements of lifetime extensions for existing reactors, often as part of the response to the current crisis … there is growing interest in the potential for small modular reactors to contribute to emissions reductions and power system reliability.